Intel Reports Q4 2020 Earnings: 2020 Delivers A Profitable Pandemic

by Ryan Smith on January 21, 2021 6:15 PM EST- Posted in

- CPUs

- Intel

- Financial Results

Earnings season is once more upon us, and once again leading the charge is Intel, who this afternoon reported their Q4’2020 and full-year 2020 financial results. The 800lb gorilla of the PC world has seen some unexpectedly strong quarters in 2020 following the coronavirus outbreak, and despite all of the uncertainty that entails, it’s ultimately played out in Intel’s favor. As a result, they’re closing the book on yet another record year, making for their fifth in a row.

Starting with quarterly results, for the fourth quarter of 2020, Intel reported $20.0B in revenue, which is a drop of $0.2B over the year-ago quarter. Intel saw a very good Q4 a year ago, and while Q4’20 is once again their strongest quarter of the year, Intel’s momentum as a whole is starting to back off on a quarterly basis. More significantly, Intel’s net income has dropped 15% YoY, with Intel booking $5.9B there.

Driving this drop – besides the ongoing market distortions caused by the coronavirus pandemic – is a combination of softer gross margins, increased R&D spending, and increased taxes. Intel’s famous gross margin remains below their historical 60% benchmark, coming in at 56.8% for the quarter as Intel continues to ramp up their 10nm capacity. Meanwhile Intel’s tax rate has shifted significantly from 14.4% to 21.8%, eating into the company’s overall net income. Still, at $5.9B for the quarter, Intel is hardly one to complain.

| Intel Q4 2020 Financial Results (GAAP) | |||||||

| Q4'2020 | Q3'2020 | Q4'2019 | Q/Q | Y/Y | |||

| Revenue | $20.0B | $18.3B | $20.2B | +9% | -1% | ||

| Operating Income | $5.9B | $5.1B | $6.8B | +16% | -13% | ||

| Net Income | $5.9B | $4.3B | $6.9B | +37% | -15% | ||

| Gross Margin | 56.8% | 53.1% | 58.8% | +3.7 ppt | -2 ppt | ||

| Client Computing Group | $10.9B | $9.8B | $10.0B | +11% | +9% | ||

| Data Center Group | $6.1B | $5.9B | $7.2B | +3% | -16% | ||

| Internet of Things Group | $777M | $677M | $1.16B | +15% | -16% | ||

| Mobileye | $333M | $234M | $229M | +42% | +39% | ||

| Non-Volatile Memory SG | $1.2B | $1.2B | $1.2B | Flat | -1% | ||

| Programmable Solutions Group | $422M | $411M | $505M | +3% | -16% | ||

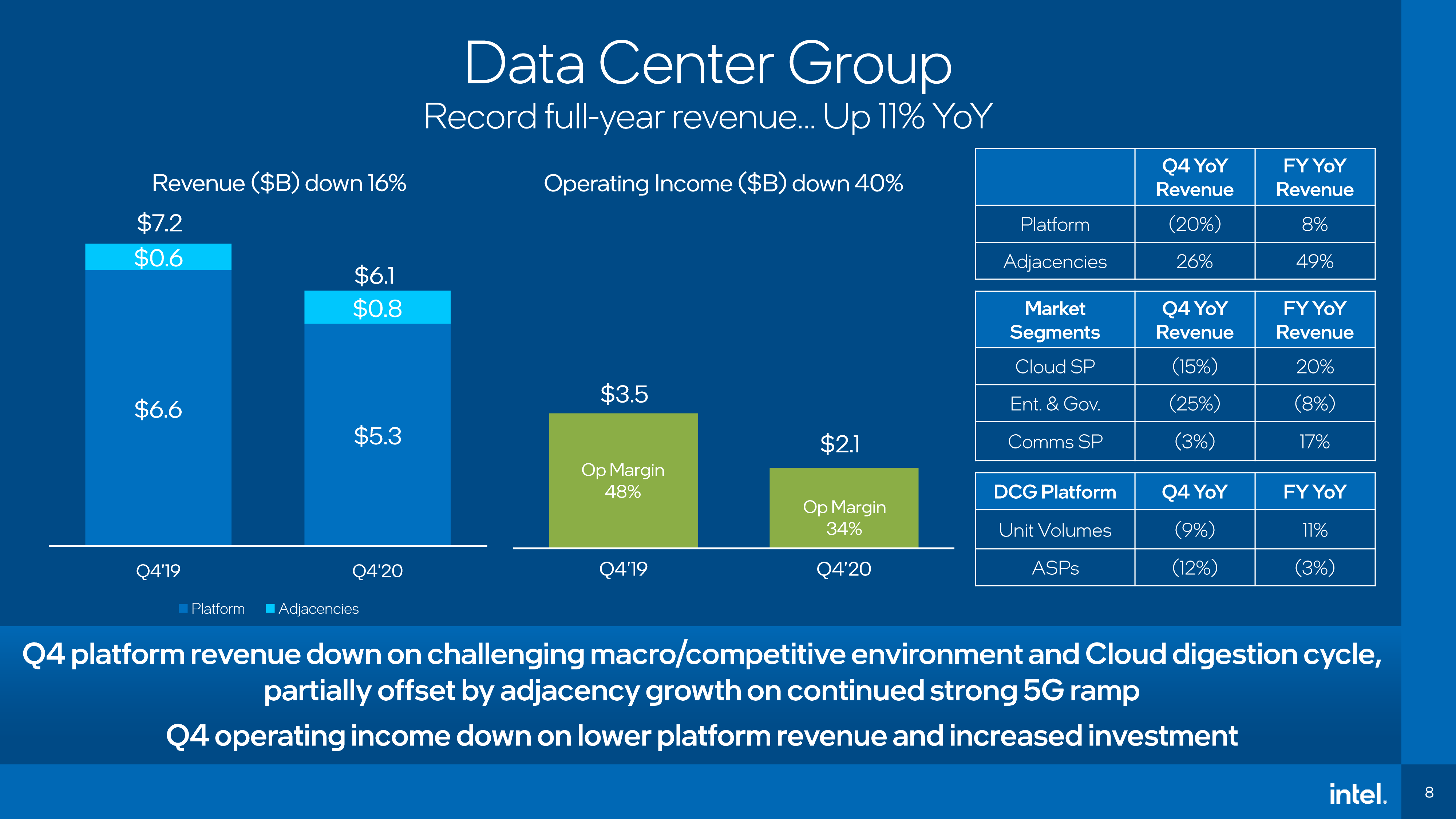

Breaking things down on a group basis, many of Intel’s internal reporting groups have shrunk over the year-ago quarter, buoyed by a handful of other groups. Data center revenue was down 16% to $6.1B, with both platform volumes and ASPs dropping versus the year-ago quarter. Intel cites the competitive marketplace and “cloud digestion cycle” for the difference, though Ice Lake Server only now shipping probably doesn’t help things.

The story is similar for Intel’s IoT, memory, and programmable solutions (FPGA) groups, all of which are down versus Q4’19. Reasons there vary from lower demand for ioT and programmable hardware, to lower ASPs on memory.

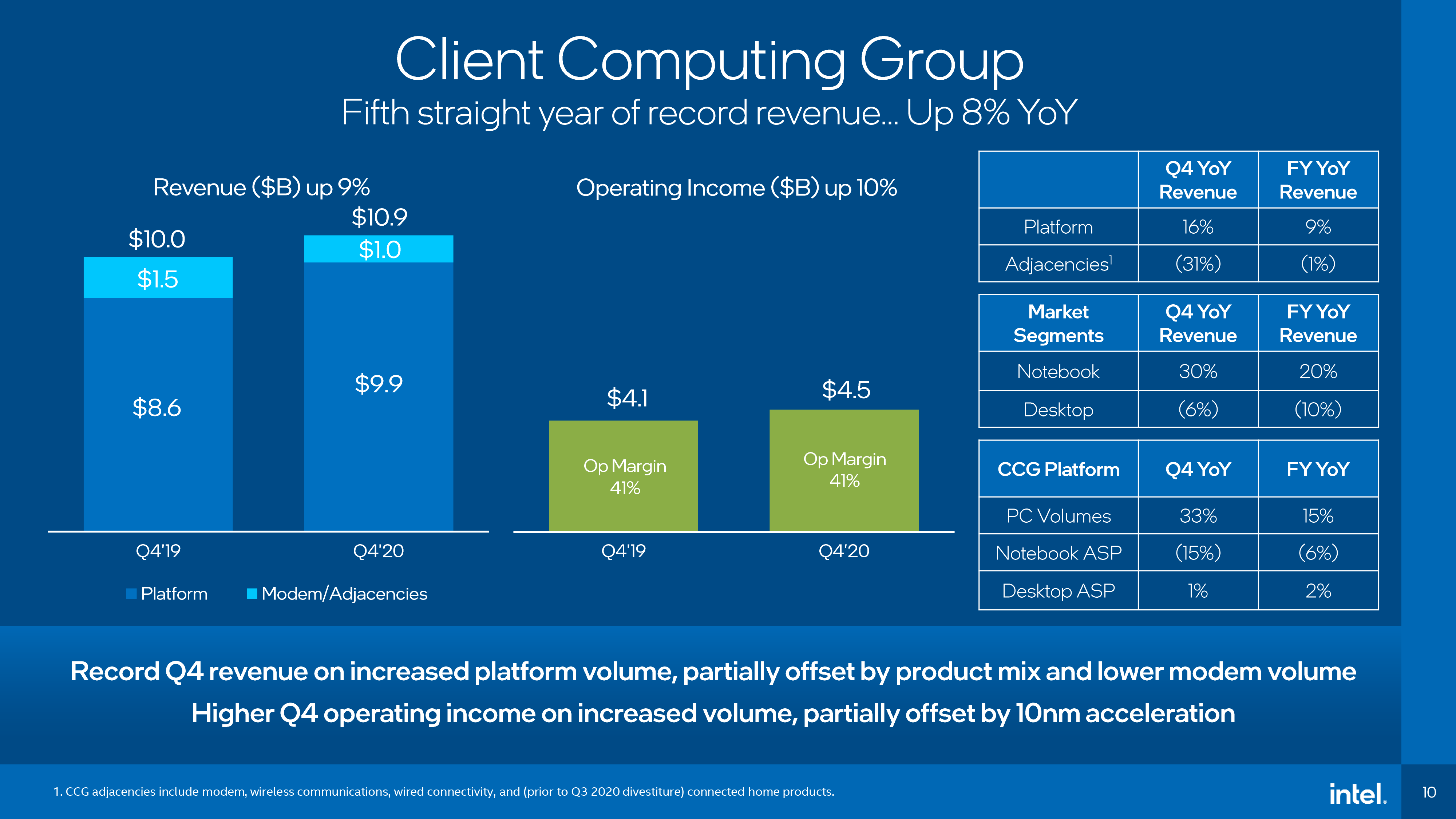

The big winner for the quarter is once again Intel’s client computing group, which was up 9% year-over-year to $10.9B of revenue for the quarter. Despite Intel’s efforts to pivot to being a data-centric company, the manufacturer’s client products remain the single largest piece of the company, so results here can make or break a quarter. In this case sheer demand for PC hardware in the face of the pandemic has driven revenue to new highs, with laptop volumes up 30% over last year. This was more than enough to offset both the drop in desktop sales – down 6% year-over-year – and a drop in laptop ASPs as consumer demand has shifted to Chromebooks and other lower-end hardware.

Full Year 2020

Shifting over to full year results, despite the initial uncertainty that came with the coronavirus outbreak, Intel ended 2020 beating expectations and setting revenue records for the fifth year in a row. Overall the company booked $77.9B in revenue for the year, 8% more than 2019. Intel’s overall net income didn’t get the same kind of kick – dogged by issues similar to their Q4 earnings – but the company is still going out on $20.9B in net income for the year, a 1% drop from 2019.

| Intel FY'2020 Financial Results (GAAP) | ||||||

| FY 2020 | FY 2019 | FY 2018 | Y/Y | |||

| Revenue | $77.9B | $72.0B | $70.8B | +8% | ||

| Operating Income | $23.7B | $22.0B | $23.3B | +8% | ||

| Net Income | $20.9B | $21.0B | $21.1B | -1% | ||

| Gross Margin | 56.0% | 58.6% | 60.2% | -2.5 ppt | ||

| Client Computing Group | $40.1B | $37.1B | $37.0B | +8% | ||

| Data Center Group | $26.1B | $23.5B | $23.0B | +11% | ||

| Internet of Things Group | $3.0B | $3.8B | $3.5B | -21% | ||

| Mobileye | $967M | $879M | $698M | +10% | ||

| Non-Volatile Memory SG | $5.4B | $4.4B | $4.3B | +23% | ||

| Programmable Solutions Group | $1.9B | $2.0B | $2.1B | -7% | ||

Gross margins for the entire year were 56%, reflecting the cost of Intel’s 10nm ramp-up and other fab matters. This was down 2.5 percentage points from 2019.

Looking at Intel’s individual business groups, for the year both the client and data center groups did very well for themselves. Client revenue was up 8% to $40.1B, coming in on the back of higher laptop sales. And that growth really is all from laptops; desktop revenue was down for the year, and even “adjacencies” (Wi-Fi adapters and the like) were down a bit versus 2019.

Meanwhile data center revenue was up 11% to $26.1B, with Intel coincidentally reporting that they shipped 11% more data center chips than in 2019. On the whole, data center growth was driven by cloud and communication service providers, both of whom ramped up their hardware purchases to meet service demands during the pandemic, while enterprise and government sales dipped on the year. Meanwhile it’s interesting to note that on both a quarterly and yearly basis, Intel’s ASPs for the data center group are down; despite the volume, they face an increasing amount of competition.

2020 was also a good year for Intel’s Mobileye and non-volatile storage groups. The automotive segment of the company continues to grow year-over-year (even with the pandemic), adding another 10% to its revenues for 2020. Meanwhile Intel’s storage business set a new record for revenue, growing on the backs of higher bit shipments as well as product launches like Intel’s “Crow Pass” 3rd generation Optane products for enterprise use.

Otherwise the laggards for the year were Intel’s ioT group and programmable solutions group. The IoT group has taken the pandemic on the chin, as IoT device sales have been soft. Meanwhile programmable solutions has been pinched by carriers’ move to 5G and overall declining revenues.

What’s Next?

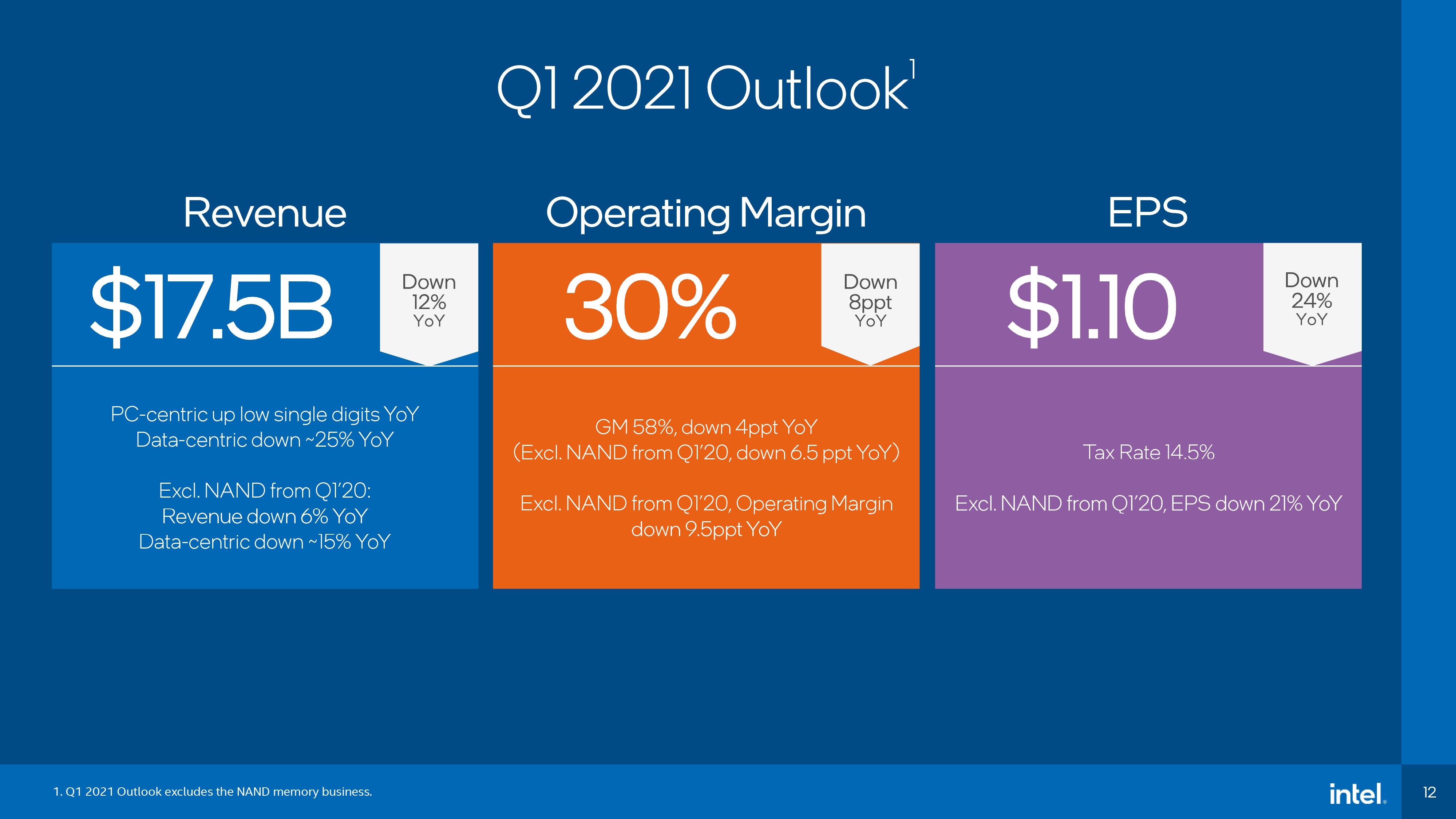

Though we tend not to focus too much on Intel’s future earnings forecasts, their predictions for Q1’2021 warrant a quick look. After 5 years of record revenues, Intel is likely to be facing some tougher years ahead, and their projections reflect this. For Q1 the company expects revenue to drop 12% versus Q1’2020. Even excluding Intel’s NAND memory business, which is being sold off to SK Hynix, and Intel is still looking at a 6% revenue drop on a yearly basis. In particular, the company expects its revenues from its data-centric businesses to drop 15%, leaving client revenue to hold the line.

The good news for Intel is that their next generation of products are close-to or have begun shipping. Rocket Lake, Intel’s upcoming desktop CPU platform, is shipping for revenue this quarter. So are Ice Lake Xeons. And the products to come after those – Alder Lake for clients and Sapphire Rapids for servers – are already both sampling to customers.

The catch, however, is that Intel is still in the midst of their fab woes. Though the company is making progress on their 7nm process, all guidance from Intel right now suggests that this process won’t be ready at scale until 2023 – two years from now. In the interim Intel will be rolling out more 10nm SuperFin capacity and their Enhanced SuperFin will follow, but Intel won’t be making a big leap forward in fab tech for their products for the next couple of years. At least, not with internally-built chips.

Previously the company had stated that they would discuss outsourcing plans as part of today’s earnings release. But following the surprise hire of Intel veteran Pat Gelsinger to be the company’s new CEO, Intel has put a pause on that announcement. The company is still evaluating the use of external fabs and will have something to announce in the future, but just not today.

In the meantime, it sounds like Gelsinger has hit the ground running. To quote our own Dr. Ian Cutress “[It] sounds like Pat already has his foot in the door. Currently in a state of transition. Feb 15th is more the date of a complete Bob [Swan] exit.” Similarly, in Intel’s earnings call today, Gelsinger commented that he’s been examining Intel’s progress on 7nm manufacturing, and that he’s “pleased” with the progress made thus far. Consequently, with 2023 shaping up to be Intel’s big year for 7nm, Gelsinger also said that he expects the majority of Intel’s 2023 products to be fabbed internally.

Source: Intel

18 Comments

View All Comments

duploxxx - Friday, January 22, 2021 - link

Does Anandtech think the good news is shiping new tech this quarter or Intel says that????There are a lot of OEM sales who advice to just skip Ice Lake because they expect a new CPU very fast as this is just an inbetween stopgap. Cascade Lake-R will continue to ship next to Ice Lake, that says enough.

Rocket Lake is to be seen if competitive with up to 8 cores... for some gamers sure the 2-3-4-5fps will do the trick to keep buying an Intel desktop on a dead platform.

In both cases ASP is down due to competition and will go down even further, because Intel had to drop prices massively and give cores for free (mainly in Cascade Lake -R to stay competitive with EPYC). Ice lake is not going to change that as they are only capable of half the core count vs AMD. 10nm HAs no longer the density and nobody is sure about the ghz scaling which was a 14nm favorits....

We as a consumer can only gain from this competition.

Deicidium369 - Saturday, January 23, 2021 - link

Of course Cooper Lake / Comet Lake will continue to sell alongside Ice Lake SP - same way Ice Lake SP will sell alongside Sapphire Rapids...Dell, HPE and Supermicro are all in on Ice Lake SP - the market for Ice Lake SP is different than for Sapphire Rapids. VM farms will not have a need this gen for PCIe5 and the added cost of DDR5 - which during a transition is always a mixed bag

Thing is - no one is buying the 64 core Epycs (top selling SKUs are 32c) - and Ice Lake SP is a shorter term platform - Golden Cove (Alder, Sapphire and un named laptop SOC) is the long term unified platform - same Golden Cove across Laptop, Desktop and Servers (1-8 sockets). Sapphire Rapids will be 4 tile - initially 14 cores per tile (out of a possible 16) each with an HBM2x stack per tile. So 56 at launch and 64 as a refresh.

10nm vanilla had/has frequency issues - big IPC uplift but offset by low clocks

10nm SF (Cobalt) has no frequency issues - the TGL H are 5Ghz - my TGL 1165G7 can hit 4.8Ghz - and one can assume that 10nm ESF (Golden Cove) will not have issues with frequency either

Intel does not need to stay competitive with AMD - it's the other way around - thing about Ice Lake SP and Rocket Lake - Intel has the advantages of being an IDM will be able to supply the materials needed for super high volume - TSMC's long fragile supply chain has already broken as it has to rely on suppliers for many more products than Intel does - and in the case of substrates - Intel has the advantage of being the substrate manufacturer's largest customer for 30 years - while TSMC has been high volume for a couple of years now (and no the 16/14/12 were NEVER in the same league as their "7nm" as far as volume) - Intel gets all they want - what's left goes to TSMC - and that goes to Apple 1st, AMD with what's left - and AMD must produce the high volume, low margin console SOCs over it's much higher margin PC CPUs and GPUs.

nobodyblog - Friday, January 22, 2021 - link

Intel Xeon sapphire lake needs to be out sooner & Intel must not finish 14nm+++, why release i3 & Pentium on non-14nm of Intel (suppose 8 cores i3 after rocket lake?)? Intel KNOWs it is still very good compared to SAMSUNG & TSMC.. do i3 on 14nm+++, Xeon & i5 & rest on 10nm++, Altera on 14nm & 10nm, etc..Deicidium369 - Saturday, January 23, 2021 - link

Sapphire Rapids will be out this year - Ice Lake SP will come first, and be made concurrently with Sapphire Rapids - both 10nm - but on separate processes (ICL is 10nm and SR is 10nm ESF).Rocket Lake is the last 14nm Desktop CPU and has been on the roadmap for a couple of years

Cooper Lake is the last 14nm Server CPUs

Comet Lake was the last 14nm Laptop SOC - both Ice Lake and Tiger Lake since both 10nm

Core i3 is going to TSMC's "5nm" 2nd half of this year and follow up to Alder Lake may be "3nm" next year. Intel 7nm is between TSMC's 5nm and 3nm.

Altera is on 10nm mostly - the newer large stuff is and has been 10nm for some time.

Habana was originally on TSMC before Intel bought it - new product was already in risk production - so Habana will stay at TSMC until next gen.

Xe HP is 10nm SF or ESF - compute card

Xe HPG is TSMC 6nm for it's initial release - and 2nd gen likely on TSMC 3nm.

Once there is 14nm excess cap - the chipsets and network cards will be on 14nm (22&28 now)

azfacea - Friday, January 22, 2021 - link

7nm is intel's last chance. if it doesnt "work right" AND "on time" AND "in great abundance". intel will have to lay off most of workforce and reinvent itself as a fabless player 10% its current size.Deicidium369 - Saturday, January 23, 2021 - link

LMAO - all 110K employees will be laid off? What are you like 12yo? - and who will provide all that fab space for 50% of the market?Get a grip. $77B+ a year company - record 5 years in a row - all the while TSMC and AMD destroying it.. LMAO

TSMC is in the middle of a crisis with not being able to secure all the items in it's long supply chain which leads to shortages - specifically of AMD CPUs and GPUs

azfacea - Monday, January 25, 2021 - link

you dont seem to be familiar with semiconductor. "who will provide ... 50% something"first of all you are delusional if you think intel makes 50% of world transistor output. 2nd the answer to your question is the next gen node.

its not 50% of world's auto output or 50% of rare earth minerals. and yes if you will have to lay off 90% of their 110k workforce if manufacturing is gone and uarch is all they have left. its called free market. it doesnt allow you to make an inferior product and pay 10 folds as many ppl.

azfacea - Monday, January 25, 2021 - link

and you showed to talk about " - record 5 year in row - " in an article you dont seem to have read.